India Paints & Building Products — sector deep-dive

The sector is running two clocks.

01Executive summary

The sector is running two clocks. The paint clock is a war: Birla Opus reached ~10% share in two years — the fastest greenfield entry in the market's history — with 1,332 MLPA of new capacity (~31% added to the industry in one cycle), pushing utilisation to ~45-50% and incumbent margins from ~18% toward ~14%. Asian Paints' June 2026 price hike (2-4%) is the first ceasefire signal, but normalisation needs Birla Opus to roughly double volumes to breakeven — a 5-7 year grind with cement 2011-16 as the precedent. The building-products clock pays now: 5.4 lakh homes complete in 2026 (decade high) and the 2022-25 launch boom delivers through FY27-29, feeding tiles (Kajaria PAT +62%, ₹297 cr buyback), adhesives (Pidilite +11%, Q4 PAT +37%), pipes (Supreme CPVC +38%, FY27 guided +15-17%) and MDF (+25.5% at Centuryply). The discipline: own the finishing wave, rent the war only where a challenger has leader-quality margins at half the price.

Why now

- The completion wave is dated and visible: homes launched 2022-25 deliver over FY27-29, and finishing materials — tiles, adhesives, bathware, panels — get consumed in the last 6-18 months before handover.

- The paint war just showed its first price discipline: Asian Paints' June 2026 hike of 2-4% signals the margin-dilution phase is moderating, with Berger/Kansai expected to follow — the FY26 prints are the trough math.

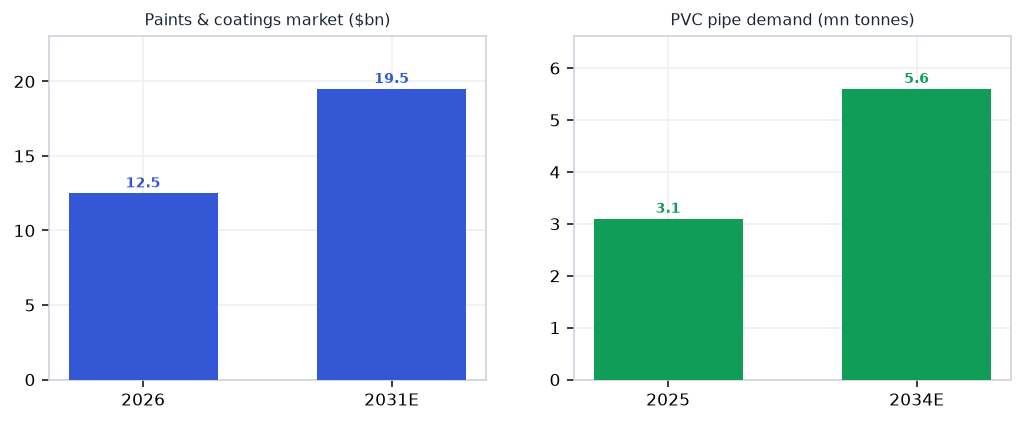

- PVC anti-dumping (~$339/t recommended) plus BIS import norms are quietly re-arming domestic pipes and panels against Chinese supply — a policy tailwind the market prices only partially.

Key risks

- Birla Opus's balance sheet can absorb losses for 4-6 years; if it targets 20-25% share, the margin war runs 3-5 more years and incumbent multiples compress even without earnings shocks.

- A resin/TiO2 cost spike (Brent >$90 or China supply disruption) squeezes paints and non-captive pipe makers simultaneously — Apollo's EBITDA −30% shows how fast it transmits.

- If real-estate demand softens, completions slip from FY27-29 to FY28-30 and the finishing-wave earnings arrive a year late at full-wave valuations.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Paints & Building Products report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Paints & Building Products opportunity in 2026?

The sector is running two clocks. The key numbers that frame the sector: ~10% in 2 yrs (Birla Opus decorative share — fastest entry ever); ~45–50% (Industry paint capacity utilisation — the glut); 5.4 lakh (2026 top-7 housing completions — decade high); +62% / +38% (Kajaria PAT / Supreme CPVC volumes FY26); 18% → ~14% (Incumbent paint EBITDA, pre-war → FY26). On the demand side, Completions 2026 stands at 5.4 lakh units — top-7 cities, highest in a decade; FY27-29 wave behind it. Together these define both the size of the Paints & Building Products profit pool and the pace at which it is compounding — the full report maps where along the value chain that value actually lands.

What is driving growth in India's Paints & Building Products sector?

The completion wave is dated and visible: homes launched 2022-25 deliver over FY27-29, and finishing materials — tiles, adhesives, bathware, panels — get consumed in the last 6-18 months before handover. The paint war just showed its first price discipline: Asian Paints' June 2026 hike of 2-4% signals the margin-dilution phase is moderating, with Berger/Kansai expected to follow — the FY26 prints are the trough math. PVC anti-dumping (~$339/t recommended) plus BIS import norms are quietly re-arming domestic pipes and panels against Chinese supply — a policy tailwind the market prices only partially. Each of these drivers is tracked in the report's catalyst section with dated windows, so readers can verify whether the thesis is playing out on schedule.

What are the key risks in the India Paints & Building Products sector?

Birla Opus's balance sheet can absorb losses for 4-6 years; if it targets 20-25% share, the margin war runs 3-5 more years and incumbent multiples compress even without earnings shocks. A resin/TiO2 cost spike (Brent >$90 or China supply disruption) squeezes paints and non-captive pipe makers simultaneously — Apollo's EBITDA −30% shows how fast it transmits. If real-estate demand softens, completions slip from FY27-29 to FY28-30 and the finishing-wave earnings arrive a year late at full-wave valuations. The full report carries an eight-item risk register scored on likelihood and severity, plus a bear-case scenario that quantifies how these risks would transmit through each node of the value chain.

Which companies are covered in India's Paints & Building Products sector report?

The report covers 24 listed companies across the full value chain (Inputs → Manufacturing → Brands → Channels → End demand), so upstream suppliers, manufacturers and downstream distribution are all graded on the same yardstick. Names screening strongest on this objective test currently include Somany Ceramics, Greenlam Industries, Apollo Pipes, Nilkamal, Greenply Industries. Every company named in the report links to its live VestAI stock page, and the universe table lets readers sort the full list on valuation, returns and balance-sheet quality.

How does VestAI grade Paints & Building Products companies?

Every name in the universe is graded on cash conversion — cumulative 3-year operating cash flow measured against reported profit. This is a data classification, not an opinion: the grade asks whether reported profits actually arrive as cash, which is where accounting-quality problems show up first. The same forensic yardstick is applied across all 30 VestAI sector reports, so a grade in Paints & Building Products is directly comparable to a grade in any other sector — and grades refresh with each quarterly data update.

Where can I read VestAI's full Paints & Building Products sector analysis?

The free version of this page includes the executive summary, key sector numbers, demand drivers, key risks and this FAQ — enough to understand how the Paints & Building Products value chain earns its money. VestAI Pro and Max members unlock the full report: the complete value-chain map with node economics, dated recent developments, the catalyst tracker, competitive structure, the scenario matrix with per-node impacts, the graded 24-company universe with an interactive comparison table, and a downloadable 15-page PDF edition. Reports are rebuilt each quarter on fresh filings, and all content is educational research rather than investment advice.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…