India Pharma / CDMO — sector deep-dive

India is the world's pharmacy — $31bn FY26 exports, 20% of global generic volumes — and the generics cash cow is…

01Executive summary

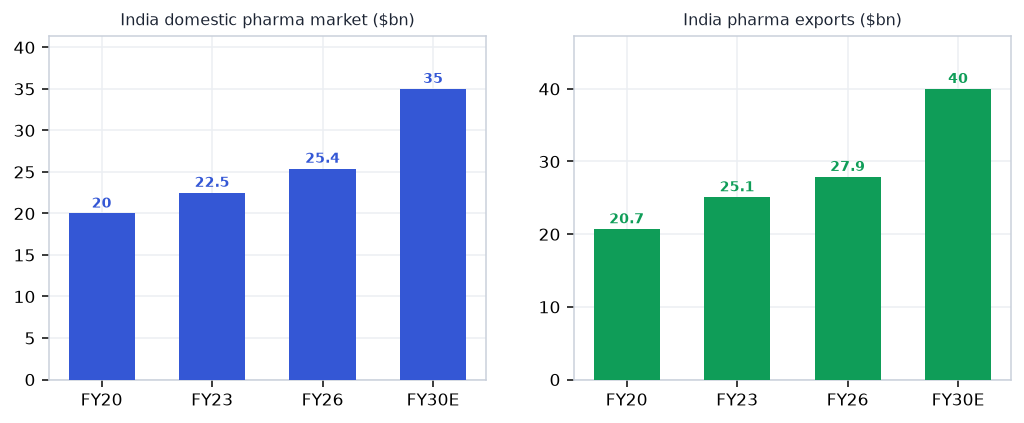

India is the world's pharmacy — $31bn FY26 exports, 20% of global generic volumes — and the generics cash cow is now funding a structural pivot into higher-margin specialty and CDMO. The US generics pricing reset is largely done; specialty/branded is rebuilding Sun Pharma's 30%+ EBITDA margins. China+1 is funnelling $8-15bn CDMO outsourcing opportunity to India's API-CDMO champions (Neuland, Syngene, Blue Jet, Laurus). Biosimilars — a $60bn+ global opportunity by 2030 — and GLP-1 peptides are the next earnings inflection. USFDA compliance overhang is easing: OAI count fell 3× in FY26.

Why now

- US generics pricing reset is mostly done — marginal improvement + specialty mix-up positions Sun/Cipla for 200-300 bps EBITDA margin expansion FY27-28 from a clean base.

- China+1 CDMO outsourcing structurally accelerating ($8.4bn→$15.4bn by 2029 at 13-15% CAGR); Neuland and Syngene (BMS to 2035) are signing multi-year anchor deals NOW.

- GLP-1/peptide wave is the next leg — semaglutide biosimilar approved India Mar 2026; 7-10 brands by FY27; India CDMO is the natural manufacture-for-world hub on peptide capacity.

Key risks

- US Section 232 pharma tariff (10-25% on imports) is the single biggest sector risk — Indian generics account for ~40% of US volumes; duty would compress margins across every large-cap.

- Concentrated CDMO client risk: Syngene ~40% revenue from BMS (even with 2035 extension); any BMS pipeline setback = immediate earnings hit — size position accordingly.

- USFDA import alert cluster risk: a single Warning Letter at a major Sun/Cipla/Reddys facility freezes US approvals for 12-24 months — monitor inspection calendars closely.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Pharma / CDMO report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Pharma / CDMO opportunity?

India is the world's pharmacy — $31bn FY26 exports, 20% of global generic volumes — and the generics cash cow is… Key figures include $31bn India pharma exports FY26 (+2.1% YoY, 20% global generic share) and 3 OAIs USFDA Official Action Indicated outcomes FY26 (down from 7 in FY25).

What is driving growth in India's Pharma / CDMO sector?

US generics pricing reset is mostly done — marginal improvement + specialty mix-up positions Sun/Cipla for 200-300 bps EBITDA margin expansion FY27-28 from a clean base.

What are the key risks in the India Pharma / CDMO sector?

US Section 232 pharma tariff (10-25% on imports) is the single biggest sector risk — Indian generics account for ~40% of US volumes; duty would compress margins across every large-cap. Concentrated CDMO client risk: Syngene ~40% revenue from BMS (even with 2035 extension); any BMS pipeline setback = immediate earnings hit — size position accordingly.

Where can I read VestAI's full analysis of the Pharma / CDMO sector?

VestAI's full Pharma / CDMO report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…