India Oil & Gas — sector deep-dive

India's gas-transition mandate is structurally underwritten: PNGRB projects demand rising from ~172 mmscmd in FY26…

01Executive summary

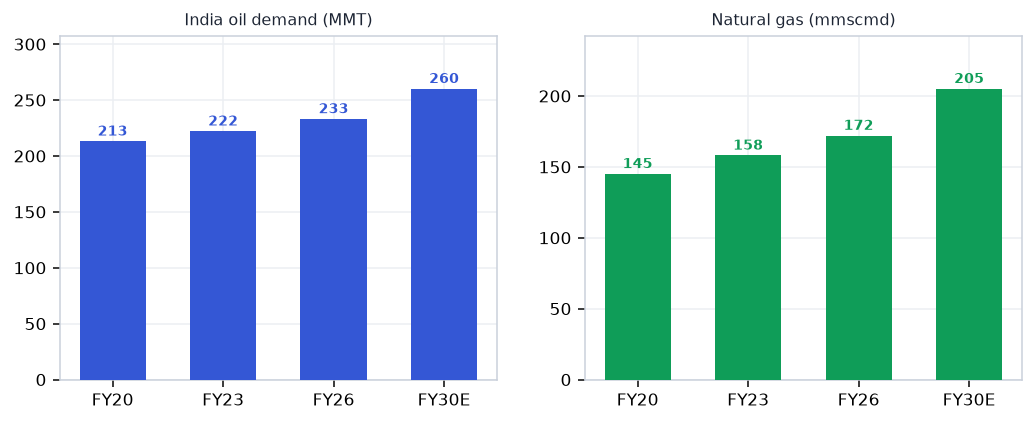

India's gas-transition mandate is structurally underwritten: PNGRB projects demand rising from ~172 mmscmd in FY26 to 297 mmscmd by 2030 (+73%), driven by CGD city-gas annuities growing 2.5-3.5x and fertiliser/power additions. Petronet LNG's Dahej expansion to 22.5 MMTPA (commissioned Mar 2026) positions India's import gateway for the next demand wave; GAIL's 18,400+ km pipeline grid (70%+ transmission share) is a toll-road compounding at 123 mmscmd. City-gas CGD concessions (IGL/MGL at 23-27% EBITDA, quarterly volume growth, monopoly GAs) and GSPL's pure-pipeline 58% EBITDA are the sector's most durable profit pools. Upstream ONGC and Oil India are cheap at 6-8x PE with 4%+ dividends but carry oil-price beta and flat-to-declining production — a value play, not a compounder. OMC refining (HPCL/BPCL/IOC) remains a trading call on GRM and crude.

Why now

- Gas-transition mandate is structurally funded and contractually live: 307 CGD areas, 12 cr PNG household target 2030, PNGRB demand projections +73% to 297 mmscmd by 2030 — city-gas concessions are monopoly annuities, not forecasts.

- Petronet Dahej expanded to 22.5 MMTPA (Mar 2026) — LNG import infrastructure is now ahead of demand; take-or-pay contracts mean Petronet earns regardless of spot LNG pricing.

- Upstream ONGC at 6-8x PE + 4% dividend with KG 98/2 production ramp as an embedded free option in FY27; below $80 crude = no subsidy burden, full cash flows pass to shareholders.

Key risks

- US-Iran peace deal + OPEC supply return could drive Brent to $60-65/bbl — every $5 fall cuts ONGC standalone PAT ~₹2,000-2,500 cr; upstream dividend sustainability is at risk below $65

- Natural Gas Supply Regulation Order 2026 industrial/commercial cuts (20%) may slow Gujarat Gas and industrial CGD volumes; CNG-to-EV substitution risk builds from FY28 as 2-wheeler EV penetration accelerates in city-gas areas.

- LNG spot prices — if Asian LNG spikes (cold winter, China demand surge), Petronet's spot sourcing margin compresses and uncontracted Dahej slots may sit underutilised; take-or-pay floor protects 17.5 MMTPA but new 5 MMTPA needs buyers.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Oil & Gas report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Oil & Gas opportunity?

India's gas-transition mandate is structurally underwritten: PNGRB projects demand rising from ~172 mmscmd in FY26… Key figures include ~172 mmscmd India gas consumption FY26; target 297 mmscmd by 2030 and 22.5 MMTPA Petronet Dahej capacity after Mar 2026 expansion (+5 MMTPA).

What is driving growth in India's Oil & Gas sector?

Gas-transition mandate is structurally funded and contractually live: 307 CGD areas, 12 cr PNG household target 2030, PNGRB demand projections +73% to 297 mmscmd by 2030 — city-gas concessions are monopoly annuities, not forecasts.

What are the key risks in the India Oil & Gas sector?

US-Iran peace deal + OPEC supply return could drive Brent to $60-65/bbl — every $5 fall cuts ONGC standalone PAT ~₹2,000-2,500 cr; upstream dividend sustainability is at risk below $65 Natural Gas Supply Regulation Order 2026 industrial/commercial cuts (20%) may slow Gujarat Gas and industrial CGD volumes; CNG-to-EV substitution risk builds from FY28 as 2-wheeler EV penetration accelerates in city-gas areas.

Where can I read VestAI's full analysis of the Oil & Gas sector?

VestAI's full Oil & Gas report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…