India Metals & Mining — sector deep-dive

India steel demand hit 164 MT in FY26 (+7.8% YoY) and is on track for 210 MT by FY30 as ₹11.2L cr of government…

01Executive summary

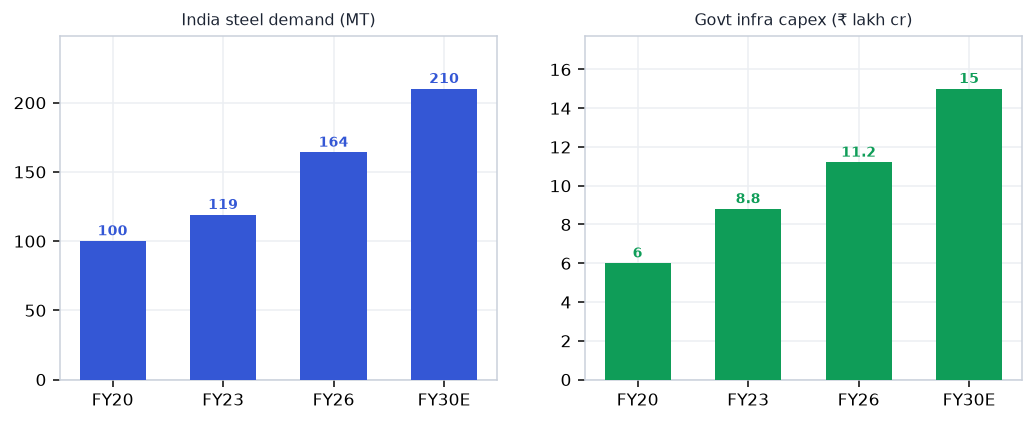

India steel demand hit 164 MT in FY26 (+7.8% YoY) and is on track for 210 MT by FY30 as ₹11.2L cr of government infrastructure capex annually — roads, rail, PMAY housing, metro — sustains the longest structural demand cycle in India's history. Yet the profit-pool is sharply bifurcated: captive-ore integrated non-ferrous players (Hindalco India aluminium at 45% EBITDA, Hindustan Zinc at 52%) and value-added downstream (APL Apollo structural tubes ~60% hollow-section market share, Jindal Stainless duopoly in SS) deliver durable compounding returns through the commodity cycle, while commodity primary steel (Tata Steel, JSW Steel, SAIL) remains cyclically exposed to China HRC dumping and imported coking-coal costs. Energy-transition metals are the emerging secular engine: India copper demand growing ~9% pa on RE/EV pull against 97% import dependence — creating structural scarcity premium for domestic plays. The investible thesis is to own captive-mine integrateds, branded value-added tubes and specialty pipe-makers for compounding returns; treat commodity primary steel as a cyclical trading vehicle and apply the gauntlet strictly on FCF, not just EBITDA.

Why now

- India steel demand 164 MT in FY26 — 10% structural CAGR locked in by ₹11.2L cr annual infra capex; NSP 300 MT target by 2030 means a decade of capacity-led investment and value-added downstream volume compounding regardless of China swing.

- DGTR anti-dumping probe on HRC (Jun 2026) + Apr 2025 safeguard duty in force — dual policy shield is the strongest import-protection wall India has built; meaningful duty outcome in H2 CY2026 could lift domestic HRC from ₹55k/t to ₹59k/t+ sustainably.

- Energy-transition metals (copper, aluminium) entering a structural deficit cycle: India copper demand compounding at ~9% pa against 97% import dependence creates captive scarcity premium for Hindalco, Gravita and Hindustan Copper regardless of global LME direction.

Key risks

- China HRC dumping persists or escalates through ASEAN re-routing even after DGTR duty — domestic flat-steel prices stay suppressed, squeezing primary-steel EBITDA margins below 13% and dragging value-added downstream input costs (APL Apollo, Welspun) simultaneously.

- Coking-coal spike above ₹280/t (85% India demand is imported) — doubles input-cost pressure on integrated primary steel players; Hindalco less exposed but JSW/Tata Steel EBITDA could compress 300–400 bps in a single quarter on a coal shock.

- Vedanta group governance risk and high promoter leverage (~68% pledge) — Hindustan Zinc earnings extraction to holdco via dividends risks HINDZINC minority-holder value; contagion risk to broader non-ferrous sentiment if Vedanta debt-restructuring escalates.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Metals & Mining report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Metals & Mining opportunity?

India steel demand hit 164 MT in FY26 (+7.8% YoY) and is on track for 210 MT by FY30 as ₹11.2L cr of government… Key figures include 164 MT India steel demand FY26 (+7.8% YoY, JPC provisional) and ₹11.2L cr Govt infra capex FY26 — steel's dominant demand driver.

What is driving growth in India's Metals & Mining sector?

India steel demand 164 MT in FY26 — 10% structural CAGR locked in by ₹11.2L cr annual infra capex; NSP 300 MT target by 2030 means a decade of capacity-led investment and value-added downstream volume compounding regardless of China swing.

What are the key risks in the India Metals & Mining sector?

China HRC dumping persists or escalates through ASEAN re-routing even after DGTR duty — domestic flat-steel prices stay suppressed, squeezing primary-steel EBITDA margins below 13% and dragging value-added downstream input costs (APL Apollo, Welspun) simultaneously. Coking-coal spike above ₹280/t (85% India demand is imported) — doubles input-cost pressure on integrated primary steel players; Hindalco less exposed but JSW/Tata Steel EBITDA could compress 300–400 bps in a single quarter on a coal shock.

Where can I read VestAI's full analysis of the Metals & Mining sector?

VestAI's full Metals & Mining report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…