India Financials — sector deep-dive

Indian banking enters FY27 with the strongest balance sheets in two decades — system GNPA at record-low 2.6%, NIMs…

01Executive summary

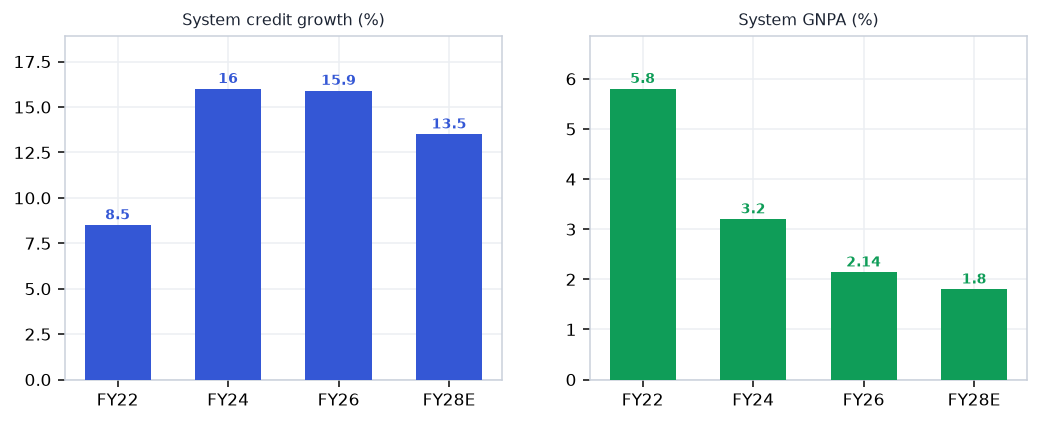

Indian banking enters FY27 with the strongest balance sheets in two decades — system GNPA at record-low 2.6%, NIMs compressed but bottoming, and the RBI having delivered 125 bps of cuts (repo now 5.25%) that structurally reduce the cost of deposits and re-price floating loan books upward over the next 18 months. The credit cycle is normalising at a healthy 13-15% system pace, but the profit-capture is sharply bifurcated: large private banks (HDFC, ICICI, Axis) trade near 5-year valuation lows on P/B, yet carry structurally superior ROEs (14-18%) and improving asset quality, while PSU banks — already re-rated 50-80% — face decelerating ROA expansion and political pricing constraints. Gold NBFCs (Muthoot, Manappuram) are the standout surprise of FY26: gold loan AUM grew 50%+ on higher gold prices + formalisation tailwind; Muthoot's NIM expanded to 12.8% and AUM hit a record ₹1.47L cr. The primary risk is idiosyncratic — MFI/unsecured stress that is contained for quality large banks but lethal for MFI-heavy NBFCs.

Why now

- Private banks trade near 5-year P/B lows despite record-low GNPA and 14-18% ROEs — the NIM compression that caused de-rating is bottoming in Q1 FY27 as MCLR reprices up.

- RBI has already cut 125 bps; incremental cuts drive deposit cost reduction 6-9 months later — Q2-Q3 FY27 NIM expansion is a near-certain catalyst for HDFC/ICICI/Axis.

- Gold NBFCs had the best AUM growth year in their history (+50%) on gold price surge + formalisation; Muthoot ROE at 24% and NIM at 12.8% — quality at a reasonable 16x P/E.

Key risks

- MFI / microfinance GNPA (currently ~5-6%) could spread to salaried and MSME segments if the monsoon-dependent rural economy weakens — would force provisioning at banks.

- RBI tightens gold loan norms (LTV cap, OTC restrictions) in H1 FY27 — could cut gold NBFC AUM growth from 40% to 15%, compressing Muthoot and Manappuram earnings sharply.

- Unsecured credit book stress at HDFC/Axis (credit cards, personal loans) — if write-offs rise above 3%, NIM recovery thesis is delayed by 2-3 quarters.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Financials report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Financials opportunity?

Indian banking enters FY27 with the strongest balance sheets in two decades — system GNPA at record-low 2.6%, NIMs… Key figures include 2.6% System GNPA — record-low, multi-decadal best (FY26 close) and 5.25% RBI repo rate post-125bps cut cycle (June 2026 MPC).

What is driving growth in India's Financials sector?

Private banks trade near 5-year P/B lows despite record-low GNPA and 14-18% ROEs — the NIM compression that caused de-rating is bottoming in Q1 FY27 as MCLR reprices up.

What are the key risks in the India Financials sector?

MFI / microfinance GNPA (currently ~5-6%) could spread to salaried and MSME segments if the monsoon-dependent rural economy weakens — would force provisioning at banks. RBI tightens gold loan norms (LTV cap, OTC restrictions) in H1 FY27 — could cut gold NBFC AUM growth from 40% to 15%, compressing Muthoot and Manappuram earnings sharply.

Where can I read VestAI's full analysis of the Financials sector?

VestAI's full Financials report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…