India Specialty Chemicals — sector deep-dive

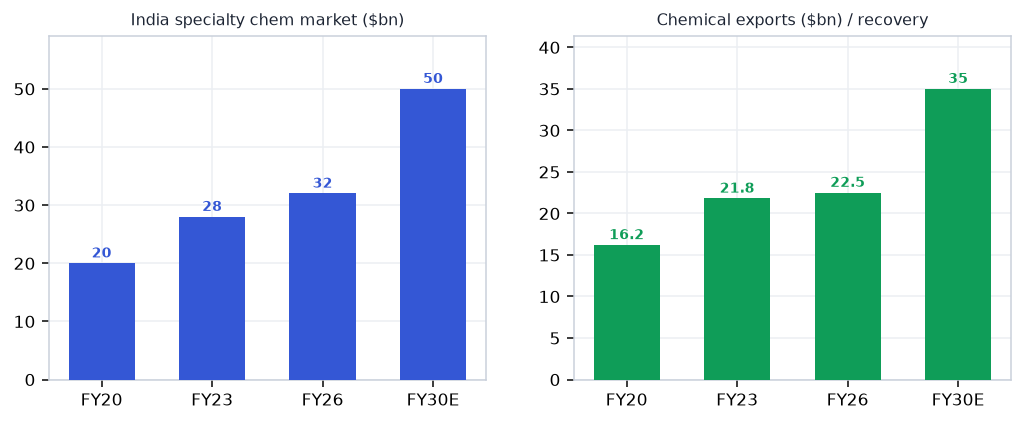

India's ~$35bn specialty chemicals market is recovering from a two-year FY24-25 downcycle driven by China dumping…

01Executive summary

India's ~$35bn specialty chemicals market is recovering from a two-year FY24-25 downcycle driven by China dumping and agrochem channel destocking. The structural China+1 shift is accelerating CRAMS/CSM order wins — PI Industries' $1.8bn CSM order book is the clearest proof point. FY26-27 is a re-rating window: agrochem inventories have normalised globally, China environmental regulations are tightening, and European REACH + US IRA procurement policies are pushing MNC pharma and agrochem majors to diversify supply chains toward India. Fluorochemicals (GFL) carry a domestic PTFE/PPA monopoly and are the cleanest EV-battery PVF demand play. Export share ~15-18% but growing — watch CSM wins, agrochemical volume recovery in H2 FY26, and China anti-dumping policy.

Why now

- Agrochem destocking is largely complete globally — H2 FY26 channel restocking lifts volumes across PI Industries, SRF, Atul and the entire agrochemical intermediate chain.

- China+1 structural shift is converting from enquiry to order — PI Industries' $1.8bn CSM book is the largest in company history; new molecule additions accelerating in FY27

- GFL holds a domestic PTFE/PPA monopoly with EV battery PVF demand inflecting 20-25% YoY — cleanest way to play India's EV growth through specialty chemistry rather than autos.

Key risks

- China resumes dumping of specialty intermediates at predatory prices — India's MRP protection mechanisms are slow; margin compression can persist 2-4 quarters before relief.

- Agrochem recovery delayed by another destocking cycle or global crop-price collapse — PI's CSM order book converts slower; ~38x PE names (Alkyl Amines) de-rate sharply.

- Concentrated customer risk in CSM — PI Industries' top-3 customers represent ~55-60% of CSM revenue; any patent expiry or molecule failure hits revenue visibility instantly.

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Specialty Chemicals report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Specialty Chemicals opportunity?

India's ~$35bn specialty chemicals market is recovering from a two-year FY24-25 downcycle driven by China dumping… Key figures include ~$35bn India specialty chemicals market size (2025) and 12-15% pa Projected market CAGR through FY28.

What is driving growth in India's Specialty Chemicals sector?

Agrochem destocking is largely complete globally — H2 FY26 channel restocking lifts volumes across PI Industries, SRF, Atul and the entire agrochemical intermediate chain.

What are the key risks in the India Specialty Chemicals sector?

China resumes dumping of specialty intermediates at predatory prices — India's MRP protection mechanisms are slow; margin compression can persist 2-4 quarters before relief. Agrochem recovery delayed by another destocking cycle or global crop-price collapse — PI's CSM order book converts slower; ~38x PE names (Alkyl Amines) de-rate sharply.

Where can I read VestAI's full analysis of the Specialty Chemicals sector?

VestAI's full Specialty Chemicals report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…