India Capital Goods — sector deep-dive

India's private capex supercycle is finally turning after a 3-year lull — CMIE new-project announcements hit ₹34L…

01Executive summary

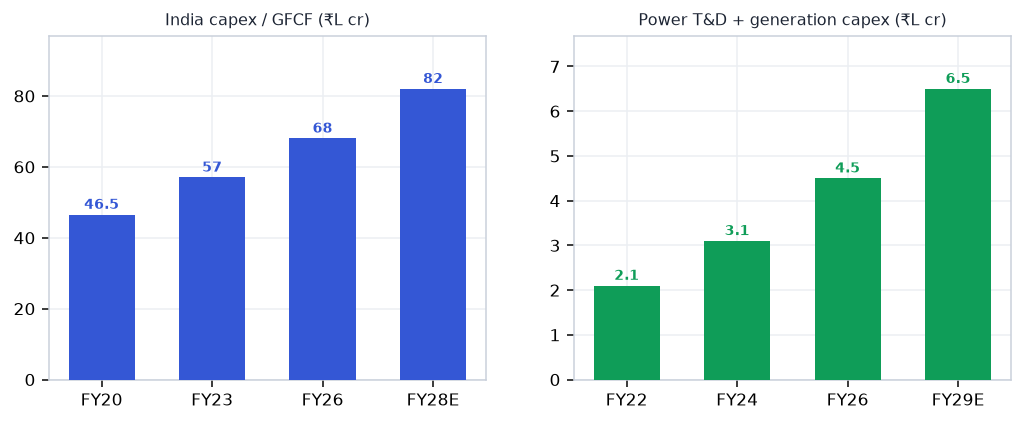

India's private capex supercycle is finally turning after a 3-year lull — CMIE new-project announcements hit ₹34L cr in FY26 (4-year high), the Union Budget commits ₹11.11L cr in capital outlay for FY27, and a $20bn data-centre pipeline is pulling high-value industrial orders from gensets to compressors to wear-parts. Manufacturing PMI has held above 57 for 8+ consecutive months, IIP capital goods printed +8% for FY26, and China+1 is delivering real export-order wins for Elgi (compressors), AIA Engineering (wear-parts) and Cummins (export gensets). Profit concentrates in IP-rich consumables (wear-parts, abrasives), branded rotating equipment (compressors, turbines) and automation — not in EPC order-book tonnage.

Why now

- Private capex is genuinely inflecting after a 3-year lull — ₹34L cr FY26 new-project announcements are the highest since FY22, led by power, chemicals and data-centres; early-cycle industrial names like Cummins and Elgi benefit before the upcycle is fully priced.

- Data-centre build ($20bn pipeline, 1→3+ GW FY27) is an entirely NEW demand layer for gensets, air-compressors and UPS — Cummins and Elgi are the two cleanest ways to own this theme without paying 80x+ for ABB or Siemens.

- AIA Engineering and Skipper offer sector-best value — both at sub-40x PE with strong cash generation, net-cash balance sheets, and structural volume tailwinds from mining wear-parts and power-grid T&D towers respectively.

Key risks

- Government capex execution shortfall — FY24 precedent shows 95% achievement is possible, but an election year or fiscal stress could cut ₹11.11L cr outlay to ₹9-10L cr, delaying T&D ordering and denting Skipper's revenue ramp.

- Data-centre project delays — the $20bn pipeline has large announcement-to-execution risk; if hyperscaler commissioning slips 12-18 months, Cummins DC-genset orders and Elgi compressed-air orders could miss FY27 guidance.

- MNC valuation de-rating contagion — ABB (80x), Siemens (65x), Thermax (55x) leave no room for earnings misses; a sector-wide re-rating on any PMI-softness could drag even reasonably-priced names like Cummins and AIA Engineering down 15-20%

02The demand engine

Where the demand comes from — the structural drivers pulling the sector's order books.

Unlock the full Capital Goods report

8 more sections — the graded universe, scenario analysis, institutional flows and the downloadable fund-grade PDF.

₹399/month · every sector report + Orion queries · cancel anytime · Already a member? Sign in

Frequently asked questions

How big is India's Capital Goods opportunity?

India's private capex supercycle is finally turning after a 3-year lull — CMIE new-project announcements hit ₹34L… Key figures include ₹11.11L cr Union Budget FY27 capital outlay (+11% YoY) and ₹34L cr Private new-project announcements FY26 — 4-year high.

What is driving growth in India's Capital Goods sector?

Private capex is genuinely inflecting after a 3-year lull — ₹34L cr FY26 new-project announcements are the highest since FY22, led by power, chemicals and data-centres; early-cycle industrial names like Cummins and Elgi benefit before the upcycle is fully priced.

What are the key risks in the India Capital Goods sector?

Government capex execution shortfall — FY24 precedent shows 95% achievement is possible, but an election year or fiscal stress could cut ₹11.11L cr outlay to ₹9-10L cr, delaying T&D ordering and denting Skipper's revenue ramp. Data-centre project delays — the $20bn pipeline has large announcement-to-execution risk; if hyperscaler commissioning slips 12-18 months, Cummins DC-genset orders and Elgi compressed-air orders could miss FY27 guidance.

Where can I read VestAI's full analysis of the Capital Goods sector?

VestAI's full Capital Goods report covers every listed name with forensic screening, quality grades and scenario analysis — available to VestAI Pro and Max members.

India's ₹25.7L cr power + transmission super-cycle through 2030 is structural — underwritten by peak-demand…

India's defence budget has crossed ₹6.81L cr in FY26 (FY27 BE ₹7.85L cr, +16%) with ₹1.86L cr capital outlay…

India ESDM market ₹3.1L cr (~$37bn) is tracking toward ₹7-8L cr by 2030, underpinned by a ₹1.91L cr PLI outlay…